Share this article

Commercial Alert

Commercial Alert Component added with 24hours no rendering once closed

Business interruption can occur due to a number of factors such as property damage caused by a major storm, flood or fire, machinery breakdowns and cyberattacks. It can disrupt or restrict operations, leading to revenue loss and potential reputational damage.

Business interruption insurance clarified

Business interruption insurance supports the recovery following a serious loss which disrupts the ability for a business to trade as normal. It provides financial protection for a reduction in turnover/lost operating income (less variable costs and any savings). It covers you from the time of the loss, through to the business recovering to pre-loss trading, or the maximum indemnity period is reached – whichever occurs first.

What does the indemnity period mean?

The indemnity period is the time (for example twelve months) in which the insurer will pay whilst you’re recovering from a major loss.

The risks of a business interrupting event in 2023

While business interruption is not a new risk phenomenon, high rates of inflation, coupled with supply chain issues, labour shortages, rising building costs, and contractor solvency, mean it now takes longer to re-instate a business premises after a serious incident. Claims, especially property claims, are also getting longer and longer to settle.

This is all seriously impacting the ability for businesses to recover quickly following a major loss. Especially when it comes to property rebuilds, which can create huge underinsurance that policyholders need to be aware of.

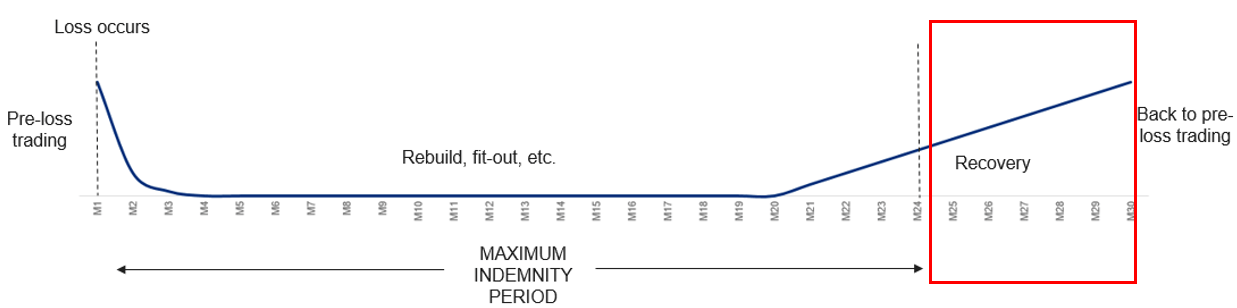

How adding just six months to the rebuild period creates significant underinsurance

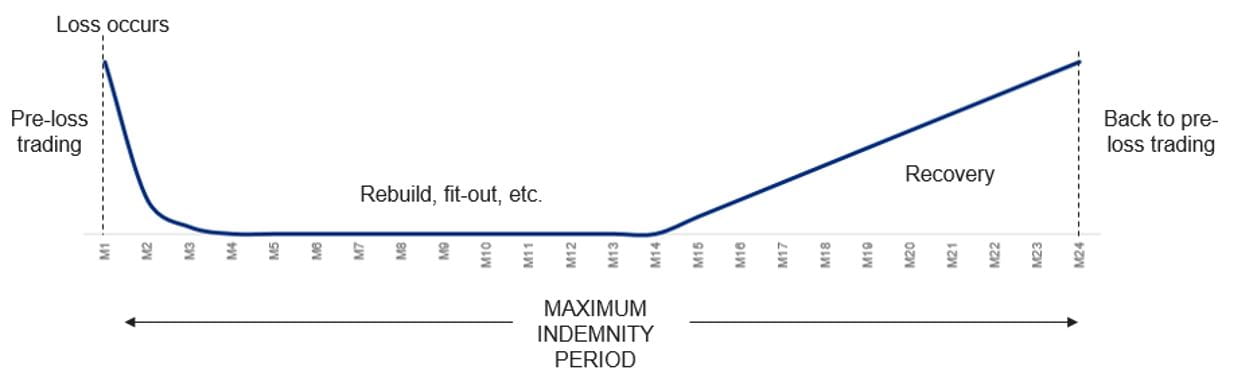

The below graph shows what typically happens following a major loss through the lens of the indemnity period (which will be stated in your policy T&Cs).

As you can see, a loss occurs and turnover reduces suddenly. It is effectively nil while rebuilding takes place. Before it starts to recover and the business eventually gets back to pre-loss levels.

The indemnity period is there to cover losses for all of that period.

Now, it’s perfectly feasible with everything in the current inflationary climate that the rebuild period is going to be prolonged.

The graph below highlights how just a six month extension to the rebuild period can affect your insurance.

As you can, the six month rebuild extension has created a period of revenue loss that is now uninsured as it is no longer covered by the indemnity period.

That’s why it is so important to look at the indemnity period in your insurance policy. You want to protect your income and your ability to trade, longer term while a rebuild is going on.

The impact of inflation on the supply chain

While inflation has huge impacts on property rebuilds, it’s not just buildings it effects. Inflation is impacting the supply chain too, particularly with sourcing new/replacement parts for machinery, raw material costs and stock levels.

When it comes to a major loss, we expect there to be a long line of contractors and suppliers queueing up to effect repairs. The reality is somewhat different, particularly in the current climate, where the lack of raw materials is a huge issue. We only have to look at the automotive industry in recent times where the lack of semi-conductors has almost brought the supply of new vehicles to a standstill. Building materials are no different, where supply challenges have been commonplace further complicated by labour shortages.

The energy crisis globally also impacts on availability of resource as does the ongoing raft of strikes within the UK population. We are all acutely aware of strike action within the railway system impacting on the movement of people and goods and there is further potential for strike action impacting on the import/export sectors.

The message here is simple, work with your broker. Explore and understand the landscape when it comes to business interruption cover and particularly, the adequacy of indemnity periods.

How to stay financially resilient in a high inflationary environment

- Consider your property reinstatement values today - inadequate or inaccurate valuation figures puts you at risk of purchasing insufficient coverage or overpaying for what you don’t need. And when insurers uncover valuation errors, they may deny future coverage, impose coinsurance requirements, or restrict sub-limits on your next renewal. Engage a professional to undertake those reinstatement values. At Marsh Commercial we work with Rebuild Cost Assessment to provide either: a desktop Rebuild Cost Assessment for just £105 + VAT*. Or a full site valuation service. Find out more.

- Day one protection is a must have to help protect against the effects on inflation during both the policy period and any reinstatement period

- Discuss with your insurance broker the challenges around underinsurance – in many insurance contracts there is a Condition of Average. This means that when receiving a claim for a property or business, if the insurer believes the property or business is underinsured, they can reduce the claim by the corresponding percentage). Some insurers may be willing to agree to waive the condition of average if you have a RICS valuation for example. Your broker will be able to help negotiate an average waiver on your behalf.

- Consider the adequacy of your indemnity period

- Refresh your business continuity plan - what you do in advance of a loss will help you when it happens to mitigate and reduce that period.

Here to help

The whole Marsh Commercial family is here to help you remain financially resilient. If you would like to learn more about any of the themes discussed in this article, contact your Marsh Commercial adviser or get in touch.

More of a listener? We explored this topic in our UK Business Risk Webinar (skip to 2:00) – catch up here.

Machine protection when you need it most

MACH 3-5-7 is specifically designed for operators of industrial and commercial machinery, and helps you plan for unforeseen mechanical breakdowns and production interruptions. It runs alongside your general insurance, not as a replacement, and provides far wider cover including operator error for a period of up to 7 years.

Got a burning question?

Let us know what you'd like to learn more about, your question may help others too! An adviser will be in touch to answer your question shortly.